AMERIPRISE FINANCIAL (AMP)·Q4 2025 Earnings Summary

Ameriprise Delivers Record Quarter as Adjusted EPS Jumps 16% to $10.83

January 29, 2026 · by Fintool AI Agent

Ameriprise Financial reported record Q4 2025 results, beating both revenue and earnings estimates while achieving all-time highs across key metrics. Adjusted operating EPS of $10.83 exceeded the $9.76 consensus by 1.1%, representing 16% year-over-year growth. The earnings call was delayed approximately 30 minutes due to technical difficulties.

The diversified financial services firm reached record assets under management, administration and advisement of $1.7 trillion, up 11% from the prior year. Strong client engagement drove $13.3 billion in client net flows for the quarter, representing a 4.7% annualized flow rate.

Did Ameriprise Beat Earnings?

Yes — double beat on both revenue and EPS.

Ameriprise has now beaten consensus EPS estimates in 5 of the last 6 quarters. The consistent execution reflects disciplined expense management and sustained client asset growth.

What Were the Key Highlights?

CEO Jim Cracchiolo emphasized the record performance in his prepared remarks:

"Ameriprise delivered a record fourth quarter with robust client activity, resulting in one of our best quarters for client inflows and strong asset growth. We generated all-time highs for revenue, earnings and EPS for both the quarter and the full year."

Q4 2025 Performance Summary:

Full Year 2025:

- Revenue growth: +6% (excluding unlocking)

- EPS growth: +12% to $39.34 (excluding unlocking)

- Capital returned: $3.4 billion (88% of adjusted operating earnings)

How Did Each Segment Perform?

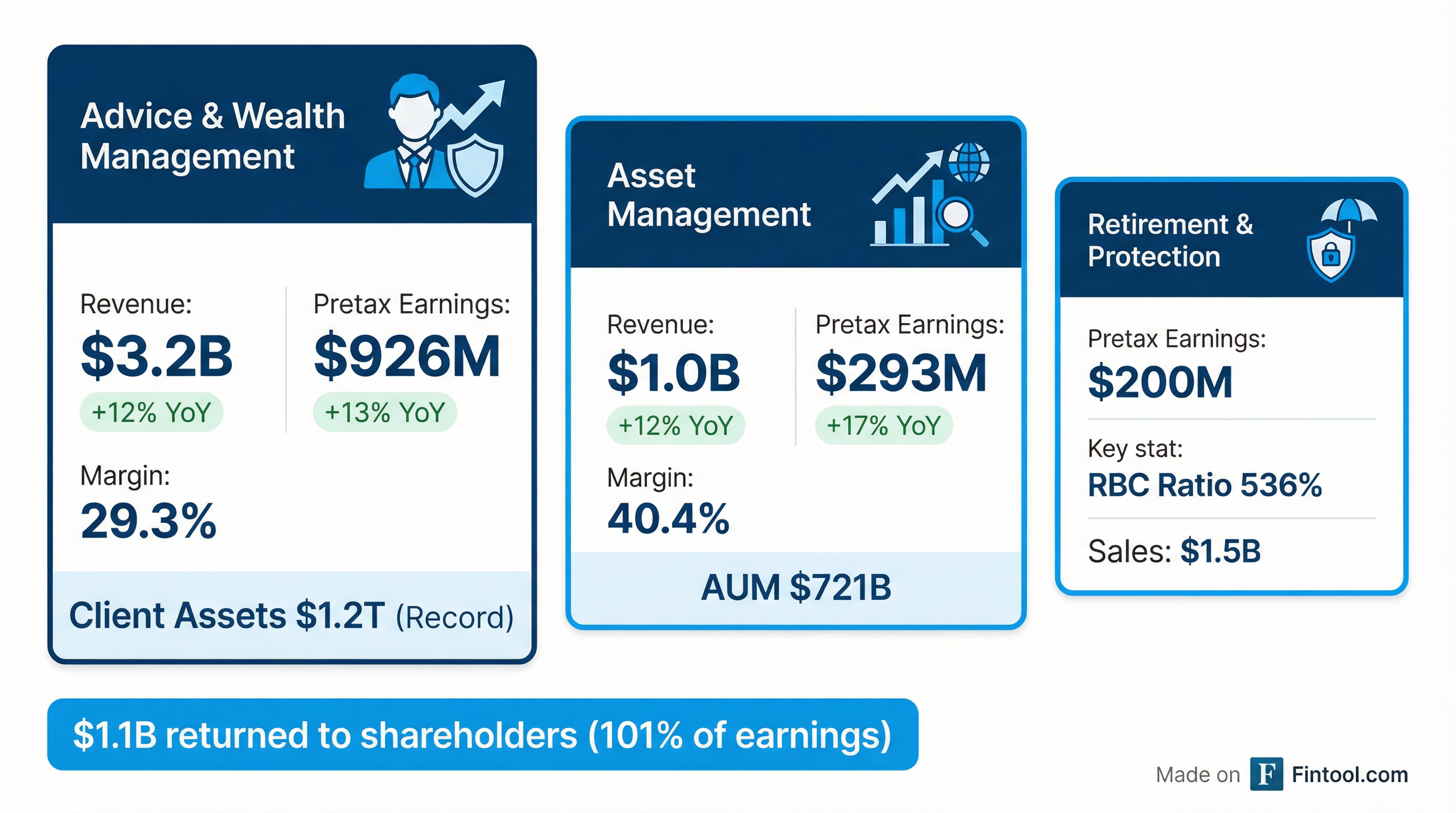

Advice & Wealth Management — Record Earnings

The wealth management business delivered record pretax adjusted operating earnings of $926 million, up 13% year-over-year, with a margin of 29.3%.

Key drivers included:

- Core earnings up in the mid-20% range, benefiting from higher client assets and well-controlled expenses

- Advisory fees increased 18% to $1.79 billion

- 91 experienced advisors recruited in the quarter

- Revenue per advisor reached $1.12 million TTM, up 8%

- Bank product expansion: HELOCs launched with strong early interest; checking accounts just launched to round out full bank offering

- J.D. Power recognized Ameriprise for 7th consecutive year for outstanding advisor phone support

Asset Management — 40% Margin

Asset Management pretax adjusted operating earnings increased 17% to $293 million with a net margin of 40.4%.

Results included higher performance fees, while the underlying fee rate remained stable.

Retirement & Protection Solutions — Consistent Cash Flow

R&PS pretax adjusted operating earnings were $200 million, within the target range.

- Sales of $1.5 billion with continued demand for structured variable annuities

- Estimated RBC ratio of 536%

- Hedge effectiveness of 98%

- ~90% free cash flow generation

What Changed From Last Quarter?

Positive developments:

- Total AUM/AUA/AA grew from $1.66T to $1.70T (+2% sequentially)

- Cash sweep balances increased to $29.9B from $27.1B in Q3

- Bank assets grew 7% to $25.3B

- Capital returned increased to $1.05B vs $842M in Q3 (+25% sequentially)

Areas to monitor:

- GAAP net income declined 6% YoY to $1.008B due to unfavorable market impacts on derivatives and market risk benefits

- R&PS earnings of $200M were below Q4 2024's $213M due to timing of G&A expenses and higher life claim expenses

How Did the Stock React?

AMP shares showed a muted initial reaction despite the strong results:

The stock has traded down from its 52-week high of $582.05 set in late 2025, presenting potential value given the record fundamental performance.

Capital Allocation & Shareholder Returns

Ameriprise returned more than 100% of adjusted operating earnings to shareholders in Q4 2025:

The company repurchased 1.8 million shares at an average price of $474 in Q4, taking advantage of lower valuations.

Balance Sheet Strength:

- Excess capital: $2.1 billion

- Holding company liquidity: $2.2 billion

- AA- rated investment portfolio

What Did Management Guide For 2026?

Management provided specific outlook during the earnings call Q&A:

CFO Walter Berman emphasized the balance between investment and efficiency:

"While we continue to invest, we also are basically transforming our expense base, constantly evaluating and improving the way we operate. The net effect should be staying within the ranges you saw."

Q&A Highlights

Organic Growth & Flows (Steven Chubak, Wolfe Research)

The Q4 flow acceleration was driven by multiple factors. CEO Jim Cracchiolo explained:

"Our flows in the fourth quarter were very strong. It was both organic growth, new clients added, flows from current clients, as well as a pickup in recruiting. Retention was very good."

Management confirmed they expect the strong flow trajectory to continue into 2026, though with normal seasonal adjustments.

Signature Wealth Platform Update (Suneet Kamath, Jefferies)

When asked about the new Signature Wealth unified managed account platform launched mid-2025:

"We're in the early innings, but very good progress. The uptake from the rollouts we've done of previous wrap-type advisory programs is actually one of the best so far."

Key capabilities advisors value include automated portfolio monitoring, rebalancing, centralized trading, and enhanced proposals. Managed SMAs were recently added, with more capabilities coming throughout 2026.

Bank Channel & Comerica (Brennan Hawken, BMO)

On the financial institutions business and Comerica's pending acquisition by Fifth Third:

"We have a very good relationship with them. Their advisors love our platform and capabilities... I know Comerica is very positive on our relationship. But that's a decision now for Fifth Third to make."

Management noted contractual protections exist for such contingencies. They continue adding new institutions and see good opportunity despite industry consolidation.

Asset Management Transformation Timeline (John Barnidge, Piper Sandler)

When asked what inning the expense base transformation is in:

"We're probably in the later innings. We're completing the work right now, and we'll complete it sometime later this year on the back-office part. We're using AI and intelligent automation and leveraging demographics offshore. We're pretty far along."

Cash Trends & Rate Sensitivity (Craig Siegenthaler, Bank of America)

On managing interest rate exposure in the bank portfolio:

"We've minimized the amount of floating. We intend to continue to implement our strategy to invest out longer so the impact, even if rates come off, we can absorb that."

The bank portfolio now has a yield of 4.6% with a 3.8-year duration, with less than 9% in floating-rate securities.

Advisor Retention (Tom Gallagher, Evercore)

On competitive pressures in advisor recruiting:

"I continue to get notes from people who have come to us from the independents, from wirehouses, from RIAs. And they said their only mistake was not coming to us sooner. Their growth since they got here has been tremendous."

Management acknowledged it's a competitive market but emphasized their strong retention levels and differentiated platform.

What Should Investors Watch Going Forward?

Positive catalysts:

- Continued wealth management client flows at elevated levels (targeting 4-5% organic growth)

- Signature Wealth platform still in "early innings" with more capabilities rolling out

- Strong capital position enables continued aggressive buybacks (85-90% payout target)

- Industry recognition (TIME's Most Iconic Companies #48, WSJ Best-Managed)

- Asset management transformation completing in 2026 should drive further efficiency

Risks to monitor:

- Market-dependent revenue (equity market declines impact AUM fees)

- Interest rate sensitivity on spread earnings (though mitigated by longer-duration positioning)

- GAAP earnings volatility from derivatives/hedging activities

- Competitive pressure in wealth management advisor recruiting

- Comerica/Fifth Third integration uncertainty for financial institutions channel

Key Takeaways

- Record quarter — All-time highs for revenue, earnings, EPS, and assets under management

- Strong beat — Revenue +3.7% and EPS +1.1% above consensus

- Wealth management momentum — Client assets up 13%, flows accelerating to 4.7% annualized rate; targeting 4-5% organic growth annually

- Best-in-class returns — 53% adjusted operating ROE, 85-90% capital return target for 2026

- Signature Wealth early innings — Successful platform launch with more capabilities rolling out in 2026

- J.D. Power recognition — 7th consecutive year for outstanding advisor phone support; 2nd year for client support

View the full Q4 2025 earnings presentation and Ameriprise company profile for additional details.